The Hidden Cost of Buying a New Car

One of the biggest financial mistakes I’ve made over the years was buying too many new cars.

I love cars. For a long time, I had a habit of buying a new vehicle every few years. At the time, it didn’t seem like a big deal. The monthly payment fit the budget, I enjoyed driving something new, and I wasn’t paying much attention to what was happening behind the scenes.

What I didn’t fully appreciate was how much money I was losing to depreciation.

A vehicle is one of the few major purchases most of us make that almost guarantees it will be worth less every year we own it. Understanding how depreciation works can save you tens of thousands of dollars over your lifetime.

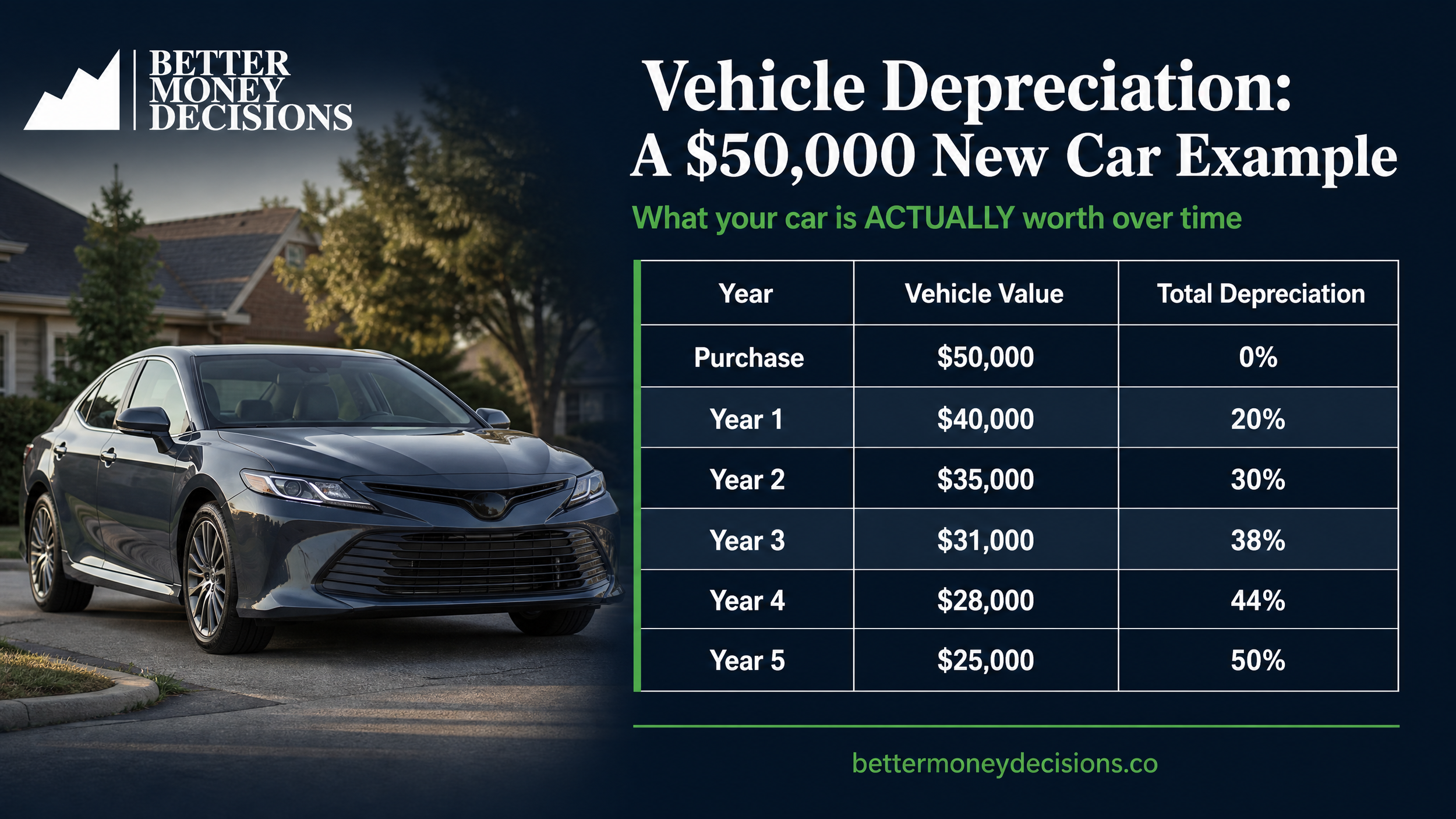

How Quickly Does a New Car Depreciate?

Most new vehicles lose value at a surprisingly fast rate.

The exact numbers will vary depending on the vehicle, but the pattern is remarkably consistent. The largest depreciation hit occurs during the first two years.

That’s why buying a brand-new vehicle can be so expensive, even if you sell it after only a short period of time.

The Negative Equity Trap

The problem gets worse when you finance a vehicle.

Let’s say you purchase a new car for $50,000 and finance most of the purchase price.

Two years later, the vehicle may only be worth around $35,000. Depending on your loan terms, you may still owe $38,000 to $40,000 on the loan.

That means you have negative equity.

In simple terms, you owe more than the car is worth.

I’ve seen people trade in vehicles with negative equity and roll that balance into the loan on their next vehicle. Many dealerships will gladly do this if the lender approves it.

In my opinion, this is one of the worst financial decisions you can make with a car.

Now you’re financing the new vehicle plus the loss from the previous vehicle. Since the new vehicle will also depreciate, it’s easy to find yourself stuck in a cycle where you always owe more than your vehicle is worth. Please never do this.

The Sweet Spot for Buying a Vehicle

This is why I believe the sweet spot for buying a vehicle is often between one and three years old. And read my post here about it.

Let someone else absorbed the largest depreciation hit, but you still get many of the benefits of buying new.

Most vehicles in this age range:

Still have modern technology and safety features

Often have remaining factory warranty coverage

Have relatively low mileage

Cost significantly less than a new vehicle

In many cases, the ownership experience is almost identical to buying new.

My Example

A six years ago, I purchased a BMW that was about a year and a half old. Yes, I know BMW’s don’t have the best history for longevity, but I love they way they drive.

It still had roughly two and a half years of factory warranty remaining. It had only about 20,000 miles on it and had all the same features as a brand-new model sitting on the dealer’s lot.

The difference was the price.

The vehicle had already depreciated by roughly $25,000. New vehicle was going for $55,000.

I essentially got the same vehicle for $25,000 less simply because someone else had owned it for a short period of time. I received 1.99% financing on the car and still driver the car today and I own the car free and clear. It’s really nice not having a car payment.

When I looked at it that way, buying new didn’t make much sense.

What I Wish I Had Known Earlier

Looking back, I bought plenty of new vehicles and traded them in after only a few years. At the time, I focused on the monthly payment and whether I could afford it.

What I should have been paying attention to was depreciation.

Every time I traded in a relatively new vehicle, I was absorbing thousands of dollars in lost value.

If there’s one lesson I’ve learned, it’s this:

Let someone else take the biggest depreciation hit whenever possible.

A one-to-three-year-old vehicle can often give you nearly all the benefits of a new car while saving you thousands of dollars.

That’s a better money decision.